The pound was little changed against the dollar on Friday as trade remained light with many markets closed for Good Friday.

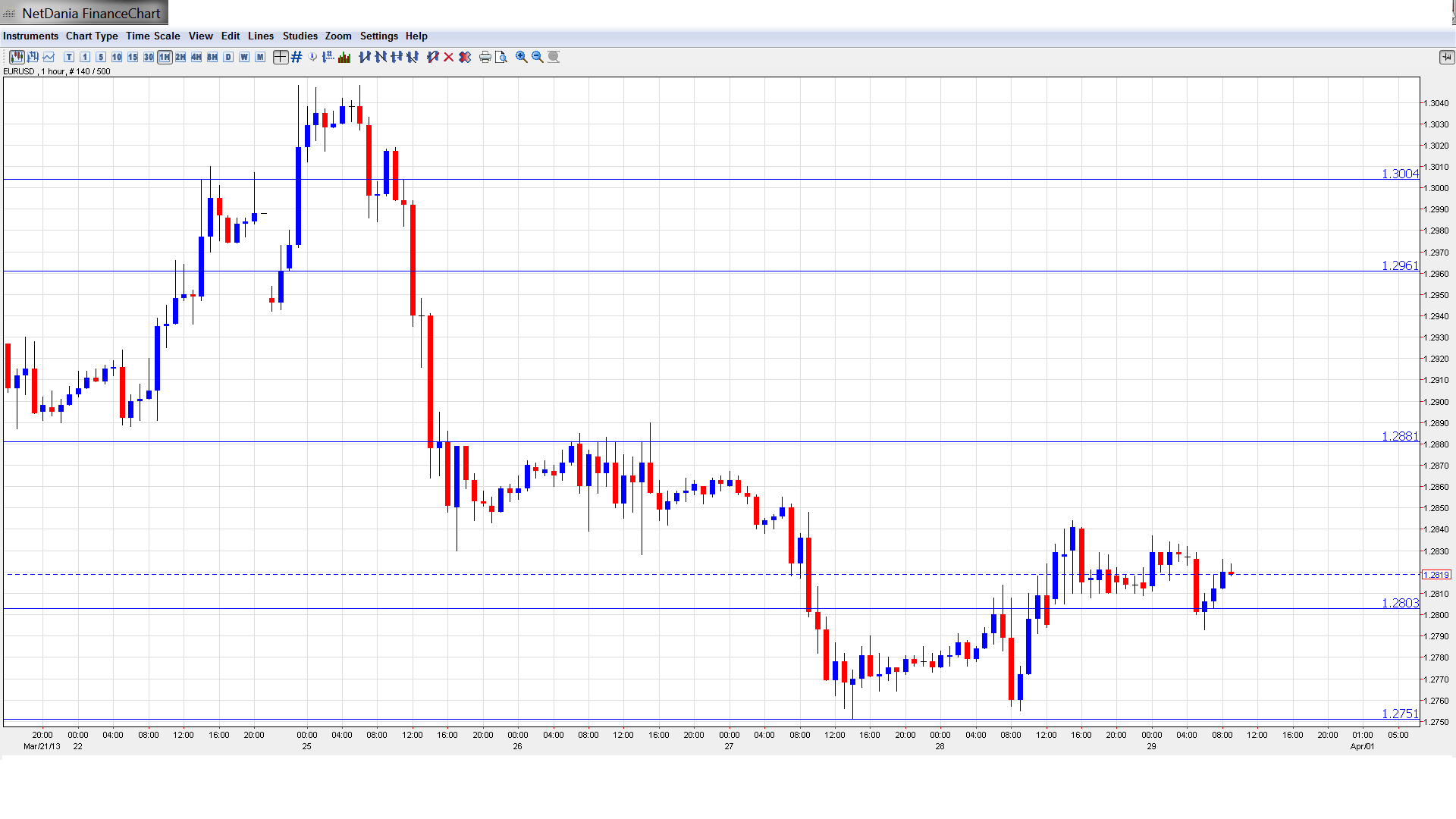

GBP/USD hit a session high of 1.5219 on Friday, before settling at 1.5190, dipping 0.02% for the day and ending the week just 0.09% higher.

Cable is likely to find support at 1.5094, the low of March 27 and resistance at 1.5258, the high of March 25.

Demand for the dollar was underpinned following the release of better-than-expected U.S. data on consumer sentiment and personal sending.

The University of Michigan's consumer sentiment index came in at 78.6, up sharply from the preliminary reading of 71.8, and above expectations for a reading of 72.5.

A separate report showed that personal-consumption expenditures in the U.S. rose 0.7% in February, the largest rise since September.

The data came one day after revised data showed that the U.S. economy expanded at an annual rate of 0.4% in the three months to December, lower than forecasts for a 0.5% expansion.

The growth rate was the slowest since the first quarter of 2011, but was higher than initial estimates for growth of 0.1%.

Safe haven demand for the greenback was also supported by ongoing concerns over the situation in Cyprus and political uncertainty in Italy.

Sterling had gained ground against the dollar on Thursday after data showing that the U.K. services sector grew at the strongest pace in five months in January eased concerns over the risk of a recession.

The Office for National Statistics said U.K. service output rose 0.3% in January, the biggest rise since August, bringing the annualized rate of output to 0.8%.

The report eased concerns over prospects for a triple-dip recession after previous economic data showed that U.K. manufacturing output fell at the fastest rate in six months in January.

In the week ahead investors will be awaiting the outcome of Thursday's Bank of England policy meeting, although the bank is widely expected to leave monetary policy unchanged. The U.S. is scheduled to release the closely watched government report on nonfarm payrolls on Friday.

Ahead of the coming week, Investing.com has compiled a list of these and other significant events likely to affect the markets.

Monday, April 1

Markets in the U.K. are to remain closed for Easter Monday.

In the U.S., the Institute of Supply Management is to release a report on manufacturing activity, a leading economic indicator.

Tuesday, April 2

The U.K. is to release a report on manufacturing activity and government data on net lending to individuals.

The U.S. is to publish official data on factory orders, a leading indicator of production.

Wednesday, April 3

The U.K.is to produce a report on construction sector activity, a leading economic indicator.

The U.S. is to release data on ADP nonfarm payrolls, which tracks private sector job creation and leads government data by two days. The U.S. is also to produce official data on crude oil stockpiles, while the ISM is to release a report on service sector activity, a leading indicator of economic health.

Thursday, April 4

The U.K. is to publish a report on service sector activity, while the BoE is to announce its benchmark interest rate and publish its rate statement.

The U.S. is to release the weekly government report on initial jobless claims. Federal Reserve Chairman Ben Bernanke is to speak; his comments will be closely watched for any indications on the future possible direction of monetary policy.

Friday, April 5

The U.S. is to round up the week with the closely watched government report on nonfarm payrolls and the unemployment rate, as well as data on average hourly earnings and the trade balance.

--> GBP/USD hit a session high of 1.5219 on Friday, before settling at 1.5190, dipping 0.02% for the day and ending the week just 0.09% higher.

Cable is likely to find support at 1.5094, the low of March 27 and resistance at 1.5258, the high of March 25.

Demand for the dollar was underpinned following the release of better-than-expected U.S. data on consumer sentiment and personal sending.

The University of Michigan's consumer sentiment index came in at 78.6, up sharply from the preliminary reading of 71.8, and above expectations for a reading of 72.5.

A separate report showed that personal-consumption expenditures in the U.S. rose 0.7% in February, the largest rise since September.

The data came one day after revised data showed that the U.S. economy expanded at an annual rate of 0.4% in the three months to December, lower than forecasts for a 0.5% expansion.

The growth rate was the slowest since the first quarter of 2011, but was higher than initial estimates for growth of 0.1%.

Safe haven demand for the greenback was also supported by ongoing concerns over the situation in Cyprus and political uncertainty in Italy.

Sterling had gained ground against the dollar on Thursday after data showing that the U.K. services sector grew at the strongest pace in five months in January eased concerns over the risk of a recession.

The Office for National Statistics said U.K. service output rose 0.3% in January, the biggest rise since August, bringing the annualized rate of output to 0.8%.

The report eased concerns over prospects for a triple-dip recession after previous economic data showed that U.K. manufacturing output fell at the fastest rate in six months in January.

In the week ahead investors will be awaiting the outcome of Thursday's Bank of England policy meeting, although the bank is widely expected to leave monetary policy unchanged. The U.S. is scheduled to release the closely watched government report on nonfarm payrolls on Friday.

Ahead of the coming week, Investing.com has compiled a list of these and other significant events likely to affect the markets.

Monday, April 1

Markets in the U.K. are to remain closed for Easter Monday.

In the U.S., the Institute of Supply Management is to release a report on manufacturing activity, a leading economic indicator.

Tuesday, April 2

The U.K. is to release a report on manufacturing activity and government data on net lending to individuals.

The U.S. is to publish official data on factory orders, a leading indicator of production.

Wednesday, April 3

The U.K.is to produce a report on construction sector activity, a leading economic indicator.

The U.S. is to release data on ADP nonfarm payrolls, which tracks private sector job creation and leads government data by two days. The U.S. is also to produce official data on crude oil stockpiles, while the ISM is to release a report on service sector activity, a leading indicator of economic health.

Thursday, April 4

The U.K. is to publish a report on service sector activity, while the BoE is to announce its benchmark interest rate and publish its rate statement.

The U.S. is to release the weekly government report on initial jobless claims. Federal Reserve Chairman Ben Bernanke is to speak; his comments will be closely watched for any indications on the future possible direction of monetary policy.

Friday, April 5

The U.S. is to round up the week with the closely watched government report on nonfarm payrolls and the unemployment rate, as well as data on average hourly earnings and the trade balance.